App Features · Jul 31, 2026

A simple financial health score designed to help you understand where you stand, what matters, and what to do next.

Your credit score was not built for you.

It was built for lenders.

It helps banks, credit card companies, landlords, and loan providers decide how risky you look on paper. That makes it important, but it also makes it incomplete.

A credit score can tell someone whether you usually pay bills on time. It can show how you use credit. It can help determine whether you qualify for a loan or what interest rate you might get.

But it cannot tell you if your monthly cash flow is healthy, if your savings habits are strong, or if you are building toward financial freedom.

That is the problem we wanted to solve with the Allo Score.

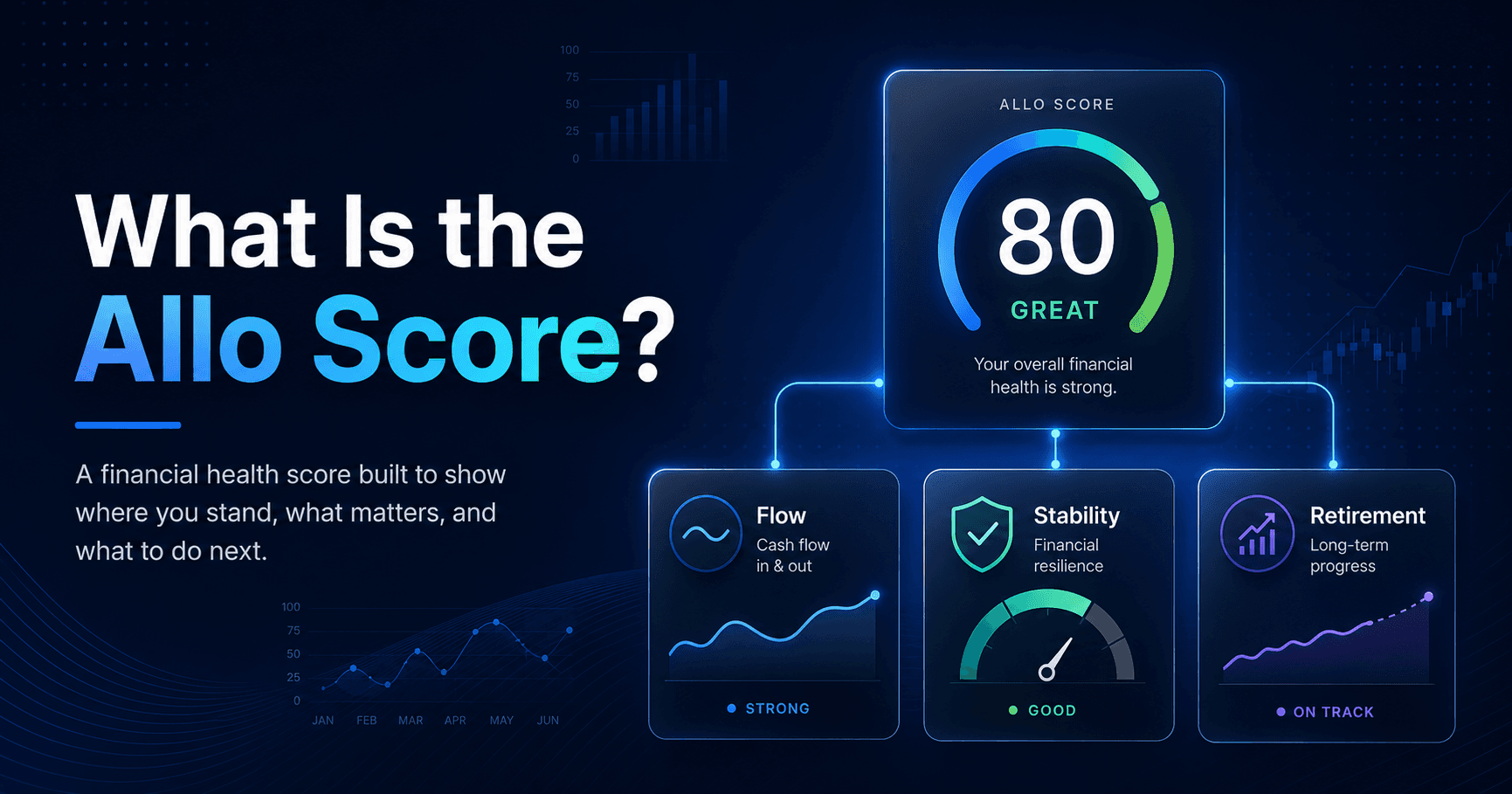

The Allo Score is a 0–100 financial health score built for the person managing the money, not the institution judging the borrower.

It is meant to answer a different question:

Is my financial life actually moving in the right direction?

Most people do not need another random number on a dashboard.

They already have plenty.

A bank balance, a credit score, a net worth number, etc.

The issue is not that people lack data. The issue is that the data rarely gives a clear answer.

You can have a strong credit score and still be living paycheck to paycheck. You can have a higher net worth because your home value increased, while your actual habits have not improved at all.

Money is connected, but most finance apps treat it like separate pieces.

The Allo Score exists to connect those pieces.

Not perfectly. Not magically. Not as some final judgment on your life.

But as a better starting point.

A way to open the app and quickly understand: here is where I stand, here is what is helping me, here is what is hurting me, and here is what I should do next.

The Allo Score is built around three major parts of financial health:

Flow. Stability. Retirement.

Those three areas matter because they cover three different questions.

Am I managing my finances correctly month to month?

That is Flow.

Can I handle pressure if life gets messy?

That is Stability.

Am I building toward the future?

That is Retirement.

A person can be strong in one area and weak in another. That is normal. That is why one number alone is not enough.

The score gives you the overview, but the categories tell you the story.

Flow is about the way you handle money across your normal monthly life.

Money comes in. Money goes out. Bills hit. Spending adds up. Savings either happens or it does not. Over time, those monthly patterns start to tell a story.

Are you keeping enough of what you earn?

Is your spending becoming easier to control or harder to manage?

Do you usually have money left over, or does every month feel tight?

Are you making room for savings, debt payoff, and long-term goals?

That is what Flow is meant to capture.

It is not just about the month you are currently in. Some parts of Flow may look across a longer period, like the past 12 months, because one month alone does not always tell the truth. A single month can be thrown off by a large bill, a bonus, a vacation, a slow work period, or an unexpected expense.

But when you look at month-to-month habits over time, patterns become clearer.

Flow includes things like savings rate, cash flow consistency, spending efficiency, and budget behavior.

A strong Flow score means your month-to-month habits are working in your favor. A weaker Flow score may mean the first issue is not your credit score, your investments, or the market. It may be the way money moves through your life month after month.

Stability is about protection.

Because life does not ask for permission before it gets expensive.

A car repair. A medical bill. A slow work month. A rent increase. A family emergency. A problem that shows up at the exact wrong time.

The question is not whether unexpected things will happen.

They will.

The question is whether your finances can absorb them.

That is what Stability is meant to measure.

At the center of Stability is your emergency fund, because emergency savings are often the first real layer of financial protection. When you have money set aside, life’s surprises are still annoying, but they do not always become financial emergencies.

A strong emergency fund gives you breathing room. It can help you avoid relying on credit cards, taking on new debt, missing payments, or having one bad month turn into a long-term setback.

That is why emergency fund coverage is one of the most important parts of Stability.

But protection is not only about savings. Stability also looks at debt pressure and credit health.

Debt pressure matters because even with money coming in, high debt payments can leave very little room to move. If too much of your income is already committed to debt, your finances can feel tight before the month even starts. The more pressure debt creates, the less flexibility you have when something unexpected happens.

Credit health matters too, but it is not the main story. Credit can affect your options, your approvals, your interest rates, and the cost of borrowing. It can open doors or create friction.

But like we mentioned earlier, credit health is only one part of being financially stable.

If your credit score is strong but your debt payments eat up your income, something is still off. If your score is improving but you have no emergency fund, you may still be fragile. If your credit is rebuilding but your debt is going down and your savings are growing, you may be healthier than the score alone suggests.

That is why Stability looks at all three together:

Emergency fund coverage shows how much cushion you have.

Debt pressure shows how much of your income is already spoken for.

Credit health shows how strong your financial options may be.

Together, they help answer a simple question:

Can your finances handle pressure?

Stability is about the cushion between you and chaos.

The stronger that cushion is, the less every unexpected expense feels like a crisis.

Retirement can feel distant, especially when the current month already has enough problems.

But the future does not get funded all at once.

It gets funded through habits.

Consistent contributions. Long-term investing. Building assets. Staying in the game. Giving time the chance to do what time does.

The Retirement part of the Allo Score looks at whether your current habits are helping your future self.

This does not mean everyone needs to have a perfect retirement plan right now. Some people are paying down debt. Some are building an emergency fund. Some are just starting to invest.

That is real life.

The point is not to shame people for where they are.

The point is to make the future visible enough that it does not get ignored.

A strong Retirement score means your long-term habits are working. A weaker one means the future may need more attention when your current situation allows for it.

The Allo Score is not meant to turn your financial life into something you obsess over.

That would miss the point.

A higher score is good, but the score itself is not the finish line. The real goal is understanding what is happening with your money and knowing what step would actually help.

If your score improves, you should know why. And vice versa.

That context matters more than the number by itself.

Because the point is not to be perfect.

The point is to be aware enough to adjust.

That is what we want the Allo Score to do: give users a clearer way to see what is working, what is slipping, and what deserves attention next.

Not as a judgment.

Not as another financial number floating on a dashboard.

But as a tool for progress.

A way to turn scattered financial signals into a clearer next step.

Because personal finance should not feel like guessing.

It should feel clear enough to act on.

Join waitlist to be first in line for launch and start taking control of your finances before everyone else.